You can still get back your tax refund.

Get your belated tax returns filed before 31st March

Capital gain is nothing but the profit that you get when you sell off a capital asset. When you sell a capital asset at a higher price than the cost at which you acquired it, you make a profit. This profit is called Capital Gain, which is your income. This income is chargeable to tax and the tax which is calculated on capital gains is called the tax on capital gains or capital gain tax.

To understand capital gains, you need to understand the concept of capital assets.

Capital assets are the property that you own and which can be transferred like land, building, shares, patents, trademarks, jewellery, leasehold rights, machinery, vehicles etc.

Here is a list of capital assets that are not coming under capital gain:–

Capital assets are divided into two types based on the period after which they are sold off. The types of capital assets are as follows –

Short term capital assets are those which are held for less than or equal to 36 months. This means that if you sell off the asset within 36 months of buying it the asset would be called a short term capital asset. However, in some cases, the period of holding is reduced to 24 months and 12 months. These cases include the following –

Long term capital assets are those which are held for more than 36 months and then sold off. Immovable property which is sold after 24 months would be categorised as a long term capital asset. In the case of equity shares, securities, mutual fund units, etc., however, the holding period of 12 months is applicable. If they are sold off after 12 months, they would be called long term capital assets.

Now that you have understood what are capital assets and their types, it’s time to understand the types of capital gains. Capital gains are also divided into short term capital gains and long term capital gains –

Short term capital gains (STCG) are the profits that you earn when you sell off your capital assets before one year of holding those. Note that the holding period varies as per the capital asset.

Long term capital gains (LTCG) are the profits that you earn when you sell off your capital assets post one year. Note that the period of holding for different assets to be claimed as long term asset varies according to the asset

Calculation of capital gains depends on the type of capital gain you are earning. Short term capital gains are calculated differently than long term ones. However, before calculating the different types of capital gains, you should understand the concept of the full value of consideration, as it forms the basis of capital gains calculation

Full value Consideration The full value of the consideration is, in simple terms, the money that you would receive when you transfer your capital asset. In technical terms, full value consideration is the consideration which the seller has received or would receive in exchange for transferring his capital asset.

Besides full value consideration, there are two other important terms:

Cost of Acquisition The Cost of acquisition is the cost price of the asset. It is the price at which you bought the capital asset.

Cost of Improvement Cost of improvement is the money spent on the capital asset to improve it. Cost of improvement is added to the cost of acquisition to compute capital gains. However, if the cost of the improvement is incurred before 1st April 2001, it would not be added to the cost of acquisition.

| Full value of consideration | xxxxx |

| Less: expenses incurred on transferring the asset | (xxxx) |

| Less: cost of acquisition | (xxxx) |

| Less: cost of improvement | (xxxx) |

| Short term capital gains | xxxxx |

Let’s understand it with an example. A house property was bought on 1st January 2017 for INR 50 lakhs. On 1st January 2018, INR 5 lakhs was spent on making improvements to the house. On 1st November 2018, the house property was sold for INR 65 lakhs.

Since the house was sold after 22 months of buying it, it would be categorized as a short term capital asset. The gain from selling the house would be called short term capital gain and it would be calculated as follows –

| The full value of consideration | INR 65 lakhs |

| Less: cost of acquisition | INR 50 lakhs |

| Less: cost of improvement | INR 5 lakhs |

| Short term capital gains | INR 10 lakhs |

| Full value of consideration | xxxxx |

| Less: expenses incurred in transferring the asset | (xxxx) |

| Less: indexed cost of acquisition | (xxxx) |

| Less: indexed cost of improvement | (xxxx) |

| Less: expenses allowed to be deducted from full value of consideration | (xxxx) |

| Less: exemptions available under Sections 54, 54EC, 54B and 54F etc | (xxxx) |

| Long term capital gains | xxxxx |

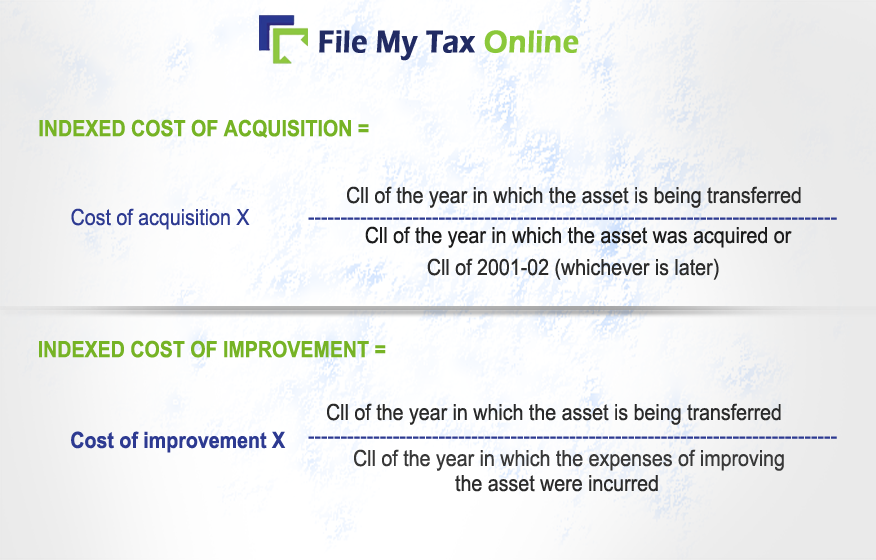

In the calculation of long term capital gains, there are three different concepts that you should understand

Indexation of costs is done to factor in inflation over the years when the capital asset is held by you. Since inflation decreases the value of money, indexation of the acquisition cost and improvement cost increases the amount of these costs thereby lowering the capital gain earned. To calculate indexation, Cost Inflation Index (CII) is used to account for the inflation incurred over the holding period. To calculate the indexed costs, the following formula is used –

With effect from the last budget (presented on 1st February 2018), the base year for CII has changed from 1981 to 2001. That is why, when calculating the indexed cost of acquisition, CII of 2001-02 is taken into consideration if the asset was purchased before the financial year 2001-02.

With the shift in the base year, the CII numbers have also changed. The CII for different years, as determined by the Central Government, are as follows –

| Financial year | Cost Inflation Index (CII) |

|---|---|

| 2001-02 | 100 |

| 2002-03 | 105 |

| 2003-04 | 109 |

| 2004-05 | 113 |

| 2005-06 | 117 |

| 2006-07 | 122 |

| 2007-08 | 129 |

| 2008-09 | 137 |

| 2009-10 | 148 |

| 2010-11 | 167 |

| 2011-12 | 184 |

| 2012-13 | 200 |

| 2013-14 | 220 |

| 2014-15 | 240 |

| 2015-16 | 254 |

| 2016-17 | 264 |

| 2017-18 | 272 |

| 2018-19 | 280 |

| 2019-20 | 289 |

| 2020-2021 | 301 |

| 2021-2022 | 317 |

These are the expenses that were necessary to be incurred when selling the asset. Without these expenses, the asset would not have been purchased. These expenses, since mandatory, are allowed to be deducted from the full value of the consideration which lowers the selling price / increases the cost of acquisition and also decreases the capital gain. The expenses which are allowed to be deducted include the following –

| Asset is a house property | If the asset is shares | In case asset is jewellery |

| . Stamp paper cost . Brokerage or commission paid to a broker for arranging a buyer . Traveling expenses incurred for sale of the asset . Expenses incurred in obtaining succession certificates, paying the executor of the Will and on other legal procedures if the property is acquired through a Will or inheritance | . Commission paid to the broker for selling the shares | . Commission paid to the broker for arranging a buyer for the jewellery |

A house property was purchased on 1st January 2000, for INR 20 lakhs. On 1st January 2005, repairs were done on the house which amounted to INR 5 lakhs. On 1st January 2018, the house was sold for INR 75 lakhs. A brokerage was paid to the broker which was INR 1 lakh. What would be the capital gain amount?

Since the asset has been held for more than 36 months, it is a long term capital asset and the gain is a long term capital gain. The gain would be calculated as follows –

| Particulars | Calculation | Amount |

|---|---|---|

| The full value of consideration | – | INR 75,00,000 |

| Less: indexed cost of acquisition | Cost of acquisition * CII of the year in which the asset is sold / CII of the year in which the asset was acquired = 20 lakhs * (CII of 2017-18 / CII of 2001-02 since it is the base year)= 20 lakhs * (272/100) | INR 54,40,000 |

| Less: indexed cost of improvement | Cost of improvement * CII of the year in which the asset is sold / CII of the year in which the asset was improved = 5 lakhs * (CII of 2017-18 / CII of 2004-05)= 5 lakhs * (272/113) | INR 12,03,540 |

| Less: brokerage paid | – | INR 1,00,000 |

| Long term capital gain | – | INR 7,56,460 |

Now that you have understood the calculation of short term and long term capital gains, it’s time to understand capital gain tax in India. Just like gains are short term and long term, capital gain tax in India is also divided into short term capital gain tax and long term capital gain tax. Let’s see the capital gain tax rate for these respective taxes –

Short term capital gains tax (STCG tax) Short term capital gains are taxed at your income tax slab rate if Securities Transaction Tax (STT) is not applicable on the gains. In such cases, the gains are added to your taxable income and then taxed at the slab rate under which your income qualifies. If, however, in the case of equity shares, STT is applicable, short term capital gains are taxed at the rate of 15%.

Long term capital gains tax (LTCG Tax) Long term capital gains are taxed at a flat rate of 20% Though STCG and LTCG are taxed at the above-mentioned rates, in the case of equity and debt-related investments, the tax rates and rules are different. Here is how equity and debt fund investments are taxed –

| Type of fund | STCG Tax | LTCG Tax |

| Equity funds (which have 65% or more investments in equity) | 15% | 10% if the gain is more than INR 1 lakh in a financial year |

| Debt funds (which have 65% or more investments in debt) | At the income tax slab rate | 20% with the benefit of indexation |

With the Interim Budget, 2019 announced on 1 Feb 2019, the tax benefits on capital gains have been widened. Extending the benefits the interim finance minister Mr Piyush Goyal pronounced that the capital gains to the extent of Rs 2 Crore can now be invested in up to two residential house properties. This is to be done in lieu of the existing provision of investment required to be made in one residential house property. But this option can be availed only once in the lifetime of the investor.

The amount so invested in these two house properties shall not attract any long term capital gains tax. The long term capital gain is presently required to be invested either in purchasing a residential house property in the next two years or constructing a house in the next 3 years or investing in bonds u/s 54EC within 6 months to make the capital gains tax free. But, from the financial year 2019-20 (the assessment year 2020-2021) the taxpayer would be made eligible to adopt this new system to invest in two residential houses once in a lifetime for an aggregate benefit of Rs 2 crore.

So, understand what capital gains are, when they are incurred, their types and how they are taxed when you are filing your income tax return. To file your taxes or get the best tax planning done, Contact us Now!!

Because capital gains tax tends to erode a significant portion of earnings, it becomes critical for individuals to utilise tax-saving strategies that would help them in reducing their tax liability. To assist individuals in minimising their capital gains tax liability, the government provides a list of exemptions under capital gains. These tax exemptions are known as capital gains exemptions.

The exemption on two house properties shall be available once in a lifetime to a taxpayer, provided the capital gains do not exceed Rs. 2 crores. The taxpayer is only required to invest the amount of capital gains, not the complete sale proceeds. The exemption will be limited to the total capital gain on sale if the purchase price of the new property is higher than the amount of capital gains.

The following conditions must be met in order to enjoy the benefit:

Exemption Under 54B: Transfer of Land Used for Agricultural Purposes

An exemption is available under Section 54B when you make short-term or long-term capital gains from the transfer of land used for agricultural purposes – by an individual, the individual's parents, or a Hindu Undivided Family (HUF) – for two years prior to the sale. The exempt amount is the lesser of the investment in a new asset or the capital gain. You must reinvest in new agricultural land within two years of the transfer date.

Exemption Under Sections 54 E, 54EA, and 54EB – Profits from investments in certain securities

This capital gains exemption applies to capital gains derived from the transfer of long-term capital assets. Individuals can take advantage of such long-term capital gain exemptions if they reinvest in particular securities such as targeted debentures, UTI units, government securities, government bonds, and so on.

The following conditions must be met–

It is important to note that any loan availed against these securities before 3 years would be treated as a capital gain.

Exemption Under Section 54EC – Profits from the sale of a long-term capital asset are exempt from tax if reinvested in specific long-term assets.

Long-term capital gains on the sale of long-term assets would be qualified for long-term capital gain exemption. Individuals will be eligible for such exemptions if they reinvest their proceeds in assets of either the Rural Electrification Corporation or the NHAI.

Such capital exemptions are available if and only if the following conditions are met:

Exemption Under Section 54EE – Profits from a transfer of investments.

Capital gains derived from the transfer of long-term capital assets would be eligible for a capital gain exemption if –

Exemption Under Section 54F: Capital gains on the sale of any asset other than a home.

Exemption under Section 54F is available when capital gains are realised from the sale of a long-term asset other than a home. To qualify for this exemption, you must invest the entire sale consideration, not just the capital gain, in the purchase of a new residential house property. Purchase the new property either one year before or two years after the previous one. You can also use the profits to fund the construction of a home. The construction, however, must be completed within three years of the date of sale.

In Budget 2014-15, it was stated that only one house property could be purchased or built from the sale consideration in order to claim this exemption. This exemption can be revoked if the new property is sold within three years of purchase. If you meet the mentioned conditions and invest the complete sale proceeds in the new house, the entire capital gain will be tax-free.

However, if you invest a portion of the sale proceeds, the capital gains exemption will be calculated as follows: capital gains x cost of new house /net consideration = capital gains x cost of new house /net consideration.

Ans. DDT stands for Dividend Distribution Tax which is required to be paid by the companies on the dividends they issue. As per Budget 2020 speech, no Dividend Distribution Tax (DDT) shall be paid by the Companies from FY 2020-21.

Ans. DDT means the Dividend Distribution Tax which is required to be paid by the companies on dividend distribution.

Ans. If the total income of the assessee including capital gains is below the basic exemption limit then no tax is levied.

Ans. There are various ways to avoid capital gains tax by investing the amount of gain in the investment schemes of the government and other methods specified by CBDT

Ans. Advance tax should be paid on capital gain income and casual incomes. The amount is calculated by adding the capital gain with total income and tax is calculated.

Ans. If the capital gains are short term, then the rate for both listed and unlisted bonds and debentures is 30% and gains are long-term, then the rate for listed bonds is 10% and for unlisted 20%

Ans. capital assets on which depreciation is charged is sold to attract short term capital gain. The cost of acquisition is taken in this case as WDV of the assets.

Ans. Short term capital gains are taxed at slab rates of the assessee. So assessees have to pay the tax on short term capital gain at its tax brackets.

Ans. It depends on the nature of the business of the assessee. If the trading of shares is the business of the assessee, then it will be taxed under business income otherwise under capital gain.

No, it cannot be avoided. The tax on capital gain is required to be paid irrespective of the residential status of the person.