You can still get back your tax refund.

Get your belated tax returns filed before 31st March

Most of us have a habit of putting off the tax filing work, unless it becomes an absolute necessity. For us missing the tax filing deadline only means filing a late return.

But, here is a note of caution for all such people!!

From last year onwards you need to be proactive and extra cautious with respect to filing of your Income Tax Returns.

Why?

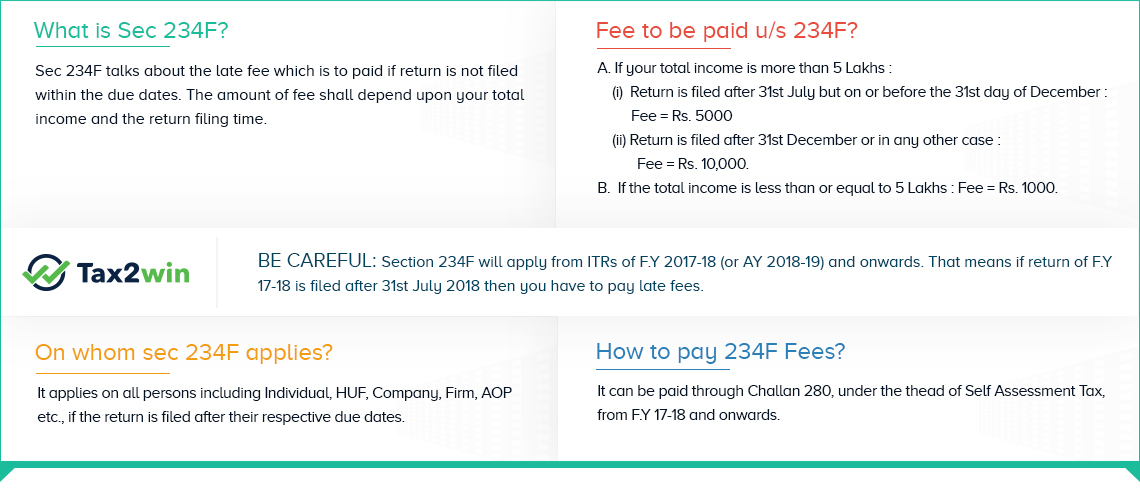

Well, From F.Y 17-18, a new Section 234F was introduced. This section imposes fees on delayed/late - filing of Income Tax Return. This penalty would be levied in addition, to the existing Interest u/s 234A for late filing of income tax return.

In this guide, we have covered each and every aspect related to the applicability of section 234F as per Income Tax Act 1961. Read carefully to avoid being the victim of section 234F penalty.

In Budget 2017 our honorable Finance Minister, Mr. Arun Jaitley introduced a new section 234F to ensure timely filing of income tax returns. As per section 234F of Income Tax Act, if a person is required to an file Income Tax Return (ITR forms) as per the provisions the of Income Tax Law [section 139(1)] but does not file it within the prescribed time limit then late fees have to be deposited by him while filing his ITR form. The quantum of fees shall depend upon the time of filing the return and the total income.

If you fall in the below conditions then you have to mandatorily file your income tax return:

Basic exemption limit is the maximum threshold amount up to which your income is not chargeable to tax. In simple words, if your income exceeds the basic exemption limit then you are mandatorily required to file the return. Currently, it is Rs.2,50,000 (for individuals below 60 years) or Rs. 3,00,000 (for individuals of 60 years and above but less than 80 years) or Rs. 5,00,000 (for individuals of 80 years and above) as the case may be

The due dates for filing Income Tax Return under section 139(1) of Income Tax Act for different categories of taxpayers are as under :

| Category | Due date of filing (FY 2018-19) | Due date of filing (FY 2019-20) |

|---|---|---|

| Individuals who are not required to be audited | 31st July 2019 (extended to 31st August) | 31st July 2020 (extended to 30th Nov 2020) |

| Company or Individual whose accounts are required to be audited | 30th Sep 2019 (extended to 31st October) | 31th Oct 2020 (extended to 30th Nov 2020) |

| Individual who is required to furnish report referred in section 92E | 30th November | 30th November 2020 |

All persons including Individual, HUF, Company, Firm, AOP etc. will be covered under the scope of Section 234F of Income Tax Act 1961. All persons will be liable to pay late filing fees, when the Income Tax Return is filed after their respective due dates.

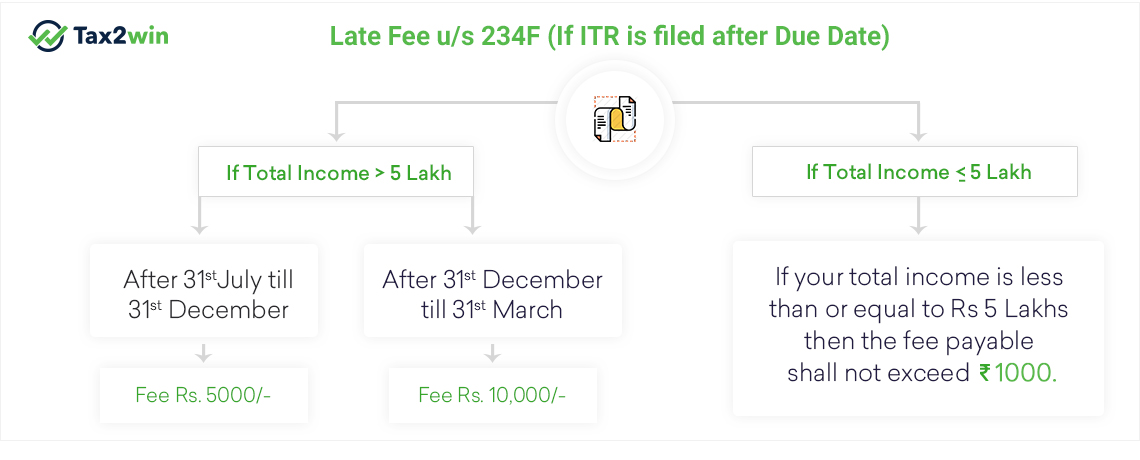

The quantum of fees that can be levied under section 234F of income tax act 1961 for FY 2018-19(AY 2019-20) filing is as under :

(i) If the return is furnished after 31st August but on or before the 31st day of December of the assessment year - Rs. 5000 (i.e 31st August, 2019 and 31st Dec, 2019 for FY 2018-19)

(ii) If the return is furnished after 31st December of the assessment year (1 Jan - 31st March) - Rs. 10,000

Example : A is a super senior citizen. His Gross Total Income for F.Y. 2018-19 is Rs. 4,95,000/-.He is filing a late return. Whether late filing fees be levied?

In the above case, late filing fees u/s 234F shall not be levied since A is a super senior citizen and his GTI does not exceeds basic exemption limit.

Let’s understand the quantum of fee that would be payable under section 234 F on the following income and return filing date through an example :

| Total Income | Income Tax Return Filing Date | Fees 234F |

|---|---|---|

| 3,00,000 | 05/07/2019 | NA |

| 6,00,000 | 31/07/2019 | NA |

| 10,00,000 | 25/07/2019 | NA |

| 25,00,000 | 10/09/2019 | 5,000/- |

| 4,00,000 | 10/01/2020 | 1,000 |

| 9,00,000 | 15/10/2019 | 5,000 |

| 4,50,000 | 13/11/2019 | 1,000 |

| 18,00,000 | 15/02/2020 | 10,000 |

The provisions of penalty under section 234F shall be applicable from 1 April 2018 i.e. in respect of Income Tax returns to be filed for FY 2017-18 (or AY 2018-19). In simple words, if we file the income tax return of F.Y 17-18 after 31st August 2018 then fees u/s 234F shall become operative. Financial year 17-18 was the first year when any such fees would be leviable without the intervention of Assessing Officer. Similarly if return for F.Y. 2019-20is filed after 31st July 2020, then penalty under 234F will be levied.

In view of improving tax compliance, it is important that the income tax returns are filed within the due dates specified in section 139(1). Therefore, section 234F has been inserted in the Income Tax Act. Further, the reduced time limits proposed for the making of an assessment under various sections are also based on pre-requisite that returns are filed on time.

As per Finance Act 2017, Late fees under section 234F can be paid by the way of "Self Assessment"---> "Others", this penalty can be paid from FY 17-18 and onwards.

Challan No. 280

Type of payment - Self assessment (300)

Fill 234 F amount in column "Others".

The fees u/s 234F shall be payable under section 140A (Self Assessment Tax). A consequential amendment has been made in section 140A to include that in case of delay in furnishing of return of income, along with the tax and interest payable, the fee for delay in furnishing of return of income shall also be payable.

Before the introduction of sec 234F, the penalty for failure to furnish the return of income was leviable under section 271F.

As per this section, if the income tax return was not filed before the end of relevant assessment year then Assessing Officer, at its discretion may levy a penalty amounting to Rs. 5,000/- However, this section has been withdrawn from the assessment year 2018-19 and onwards after coming of penalty under section 234F into force.

In order to avoid payment of late fee u/s 234F, one needs to file the income tax return on time in respect of every assessment year :-) Visit File My Tax online for hassle free ITR filing.

No, fees u/s 234F is mandatorily applicable. herefore, it cannot be waived off by income tax authority.

Yes, the income tax department will adjust the excess TDS deducted (which you would have received by the way of refund) in the payment of late fees under section 234F.

A consequential amendment in section 143(1) has been done in consonance with the introduction of sec 234F. Now, the fee payable under section 234F would also be considered in the computation of amount payable or refund due, as the case may be, on account of processing of the return.

According to the Income Tax Act, the amount payable under sec 234F is termed as late fees. But,it has been observed that in common parlance, many of us are designating the amount under sec 234F as the penalty instead of fees, which is not the case. The reason being that, this fee is steeper in nature in which the assessing officer has no role in deciding its applicability. It is automatically applied after the due date.

Even after the payment of taxes if you don’t file your IT returns then the IT department may issue a notice of non-compliance after the end of relevant assessment year and late filing fees will be levied u/s 234F.

As per section 234F the amount of fee u/s 234F shall be Rs.1000 where income is below Rs. 5,00,000.

Hence, in your case, the quantum of fees/penalty shall be Rs. 1000 if you file between the time period 1st August to 31st March. For FY 2018-19, it's from 1st September to 31st March.

As per section 234F, for individuals having income above Rs. 5,00,000 and filing the return before 31st December of the assessment year then the amount of fee shall be Rs.5,000. Hence, in your case, the quantum of fees leviable shall be Rs. 5,000.

As per section 234F, for individuals having income above Rs. 5,00,000 and filing the income tax return after 31st December but before 31st March of the assessment year then the amount of fee shall be Rs.10,000. Therefore, in your case, the quantum of late fees leviable shall be Rs. 10,000.

No, it is not possible to file the income tax return for F.Y 17-18 after 31st March 2019. Finance Act 2017 brought an amendment under the time limit of section 139(4), you cannot file your return after the end of relevant assessment year.

No, as per section 234F, the penalty shall be levied on late filing of return but not on late e-verification of return.

Hence, If you e-verify after the due date of filing return but before 120 days of filing the return, fee u/s 234F cannot be levied.

Yes, fee under section 234F shall be levied even if TDS has been deducted by your employer. The reason being that fee under 234F is levied in respect of timing of return filing and not in relation to the payment of taxes.

Yes, fee under section 234F shall be levied even if TDS has been deducted by the bank and your total income is more than the basic exemption limit.

As fees under section 234F is levied in respect of timing of return filing and not in relation to the payment of TDS.

Yes, penalty under Section 234F would be leviable in your case. In your case, you are required to file ITR as per law because your income before deductions is above the basic exemption limit. Therefore, if you file the belated return then sec 234F shall be applicable. Late Fees of Rs. 1000 shall be applicable in your case.

No, if your income before deductions falls below the basic exemption limit and you are not required to file income tax return but still if you file the belated return then sec 234F penalty shall not be applicable.

No, fees u/s 234F shall not be applicable in your case if your income is below exemption limit or nil and you are filing the belated income tax return.

Yes, both will be applicable simultaneously in a situation when your tax is payable. However, in case of late filing of return when no tax is payable then interest under sec 234 A shall not be levied and only late fee u/s 234F shall be leviable.

Just don’t get confused in both of these sections. Sec 234A speaks for levy of interest at the rate of 1% on the tax amount due while section 234F talks about levy of a definite amount of late fees depending on the date of filing of the return.Therefore, both will be applicable in case of delay in filing of return u/s 139(1) if your tax is unpaid.

In this case, after the e-verification of return, it would be processed by the income tax department as per the normal provisions of the income tax law.

No there is no such exemption of penalty under section 234F. The conditions of levy and the quantum of fees remain the same in case of every individual including super senior citizen.

Yes, even if you are eligible to receive the refund in ITR of F.Y 2018-19 and onwards still late fees u/s 234F shall be applicable in your case as per the applicable provisions.Further, the Income Tax department shall first adjust the fees and then the interest( if any) from your refund amount.

Section 234F becomes applicable to an assessee when he/she is compulsorily required to file an income tax return & files income tax return after 31st July, 2019 (now extended till 31st August, 2019).

Section 234E levy late fees on delay in submitting TDS return after the relevant due dates. While on the other hand, Sec 234F levy late fees on filing income tax return after 31st July, 2019 (now extended till 31st August, 2019).

Section 139 of Income Tax Act 1961 defines different types of income tax return which can be filed by various assessees. Like mandatory/ voluntary return u/s 139(1), loss return u/s 139(3), belated return u/s 139(4), revised return u/s 139(5), income tax return of a charity or religious institution u/s 139(4A) etc.

Section 271F imposes penalty on failure to furnish income tax return till the end of relevant AY at the discretion of assessing officer. But, from 1st April, 2017 Section 271F has been abolished & new late filing fee under Section 234F has been introduced.

Section 234D levy interest on excess amount of refund given to the assessee. When a refund is given to an assessee as per Sec 143(1) & later it is found that either refund was not due or excess refund has been given. Then on such excess tax refund, interest @ 0.5% per month is to be paid.

Section 234A levy interest on delay in filing of income tax return @ 1% per month. You can read more about Sec 234A, Sec 234B & Sec 234C in our blog.

Income tax return can be filed FREE of cost by the assessee by making self-assessment.In case, any consultation is needed for tax saving & planning then consultation charges are required to be paid.

Gross Total Income is the total of all five heads of income namely Income from Salary, Income from House Property, Income from Business, Income from Capital Gain and Income from Other Sources.

Whereas Total Income is the income which is computed after subtracting all deductions under Chapter-VIA like life insurance premium, contribution to PPF, contribution to NPS etc. from the Gross Total Income. In other words, it is the amount of income which is offered for tax and that’s why it is also known as taxable income.