You can still get back your tax refund.

Get your belated tax returns filed before 31st March

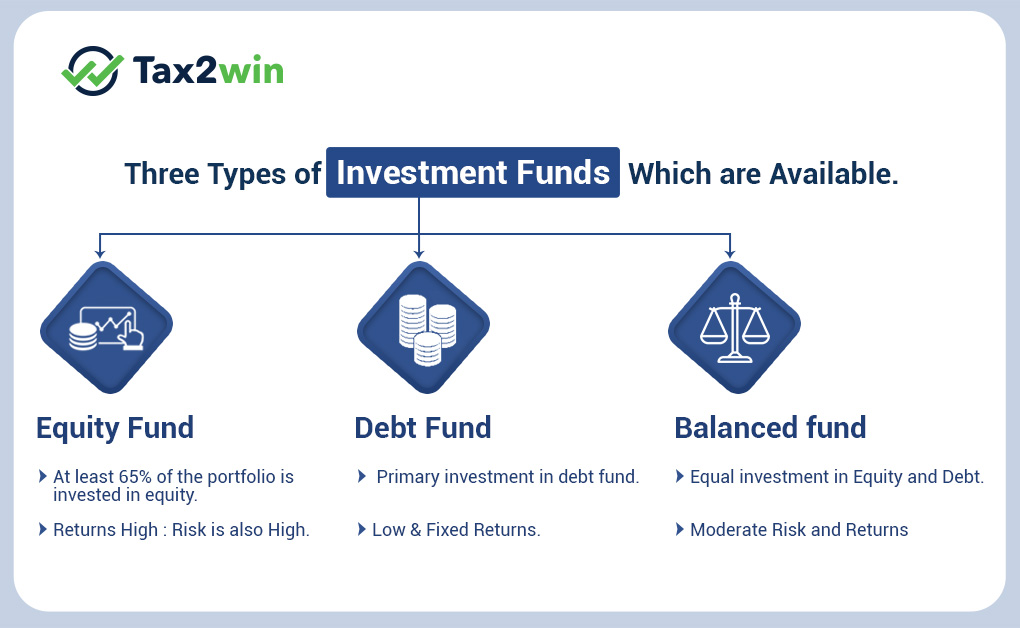

You have the flexibility of choosing the fund into which you want to invest your premiums. You can invest the premium in any one or more of these funds as per your investment strategy.

NAV = Total market value of investments of the fund’s portfolio / number of securities bought by the fund

ULIPs are mainly of three types which are as follows –

Savings/Endowment ULIPsUnder these plans, the primary objective is wealth creation. You choose the plan tenure, the premium amount, the sum assured and the investment fund. You pay the premiums which are invested in the chosen fund and then you can let your investments grow.

Child ULIPsChild ULIPs are child insurance plans whose main aim is to create a corpus for the child even if the parent is not around. Under these plans, insurance cover is, usually, on the life of the parent. If the parent dies during the term of the plan, the plan does not terminate. There is an inbuilt waiver of premium rider due to which the future premiums of the plan are waived off and the plan continues till maturity. The insurance company pays the premium on behalf of the deceased parent. Thereafter, when the plan attains maturity, the fund value is paid. Child ULIPs, therefore, help in creating a corpus for the child’s future through market linked growth.

Pension ULIPsPension ULIPs are life insurance deferred annuity plans. You buy a plan with a specific term. During the policy term premiums are payable which accumulate into a corpus with market-linked returns. Once the term of the plan is over, the accumulated corpus is then used to buy annuities. Annuities are regular incomes which are paid to the policyholder till his lifetime. Thus, pension ULIPs create a substantial retirement fund and help in generating income after retirement.

ULIPs are different from other life insurance plans because they provide you with various unique benefits which make the plan very flexible in nature. These unique features are as follows –

Partial withdrawalsPartial withdrawals allow you to withdraw from your fund value partially. After the lock-in period of 5 years is over, your fund value can be used for meeting urgent financial needs. Through partial withdrawals, ULIPs allow you easy liquidity. There is a limit to the amount of partial withdrawal which you can do from your fund value. Usually, ULIPs require you to maintain at least one annualised premium in the fund value at all times after doing a withdrawal.

SwitchingSwitching means to transfer your invested premium from one fund to another. Once you choose a fund for investing your premium, the choice is not fixed in nature. You can change investment funds whenever you want through the switching facility. Switching, therefore, lets you change investment strategies as per market movements. For instance, if you have invested in debt funds and the equity market is growing, you can switch your fund value from debt fund and transfer it to equity fund to bank in on the growth. Similarly, if the equity market is volatile and you want to protect your investments, you can switch your investment from equity fund to debt fund. Switching is allowed without any limits.

Top-upTop-up is an additional premium, over and above the actual premium paid under the plan, which you want to invest in your unit linked plan’s fund. When your ULIP is giving you very good returns, you might want to increase your investments to generate higher returns. Top-ups allow you to increase your investments through the payment of additional premiums. Moreover, every top-up that you make in your unit linked plan would also have a sum assured. Thus, top-up investments would also increase your plan’s aggregate sum assured level as well as fund value.

Premium redirectionPremium redirection is like switching but with a difference. While in switching you take out your investment from one fund and transfer it to another, in case of premium redirections, future premiums are redirected to another fund. Thus, the earlier premiums which were paid continue to remain invested in the funds which you selected earlier. Only new premiums are redirected to be invested in another fund.

Settlement OptionSettlement option is allowed when the plan matures. Through the settlement option the policyholder is given the choice to avail the maturity proceeds in five equal instalments over five years after maturity. So, if the fund is performing well and you want to continue to remain invested in the plan, you can choose to take the maturity value in instalments leaving the fund value in the fund to grow over the next five years.

As stated earlier, various charges are deducted from the fund value in a unit linked plan. These charges include the following –

Premium allocation chargeThis is the first charge which is deducted from the premium before it is invested in any fund. The premium allocation charge represents the commission paid to the insurance middleman for selling the policy and bringing in the premium. The premium allocation charge is the highest in the first year and thereafter reduces in subsequent years. After a few years, the charge becomes nil.

Policy administration chargeThis charge is deducted for maintaining the policy. Administrative charges are directed from the fund value every month.

Fund management chargeThe fund in which the premium is invested is managed by expert fund managers so that the investment can reap maximum returns. These fund managers are paid a fund management fee which, in turn, is deducted from the fund value in the form of fund management charges

Mortality chargeThis charge is deducted for the insurance cover provided under the plan. The mortality cost covers the death risk and is deducted from the fund value.

Discontinuation chargeUnit linked plans have a lock-in period of 5 years. If the plan is surrendered during the lock-in period, discontinuation charges would be levied. The charge would be deducted from the fund value and the fund value would be transferred to a discontinued policy fund. The fund value would remain in the discontinued policy fund till the completion of five years after which the value would be paid to you.

Other chargesBesides these common charges, there are other charges which might be levied which include the following –

ULIPs, like any other life insurance plans, give tax benefits. These benefits are as follows –

On premiums paidThe premiums that you pay for the unit linked plan are allowed as a deduction under Section 80C. The limit of deduction under Section 80C is up to INR 1.5 lakhs. Premiums paid for pension ULIPs qualify under Section 80CCC. The limit under Section 80CCC is also INR 1.5 lakhs including Section 80C limit. However, for premiums to be eligible as deductions under Section 80C or 80CCC, the following parameters should be fulfilled –

If the policy is surrendered after the completion of the first 5 years of the policy, the surrender value received is completely tax free.

The maturity benefit received is completely tax free in your hands under the provisions of Section 10 (10D). However, the sum assured should be at least 10 times the annual premium. For instance, if the premium is INR 1 lakh, the sum assured should be INR 10 lakhs and above for the maturity benefit to be tax-free under Section 10 (10D). If the sum assured is not up to at least 10 times the premium, the entire maturity benefit would be taxable in your hands. So, in the example, if the sum assured is below INR 10 lakhs, the maturity proceeds would be taxable at your slab rates in your hands.

The death benefit, however, is completely tax free if the insured dies during the term of the plan. In case of death benefit the sum assured need not be at least 10 times the annual premium. Whatever benefit is paid by the insurance company would be tax-free in the hands of the nominee.

ULIP is a life insurance product which is given to the holder to cover the risk. Along with this, the holders can achieve twin benefit of making investment of money in other qualified investments like bonds, mutual funds, and stocks.

According to the data, some of the best unit-linked life insurance of 2019 are Aegon Life Maximise Secure Plan, Bajaj Allianz Future Gain, PNB MetLife Smart Platinum, SBI Life Wealth Assure, LIC Market Plus – I Growth Fund are some of the best plans available.

For ULIP, a customer has to pay fund management charges along with allocation charges, administration charges, mortality charges, and in some cases guarantee charges.

SIP is just a method of investing in mutual funds whereas ULIP provides risk cover (benefit of insurance) as well as an opportunity for investments.

An endowment policy is a contract which demands payment either upon reaching maturity or on death.

Initially, the minimum lock-in period of ULIP was 3 years which has now been increased to 5 years. This will lead to an equal distribution of charges over a period of 5 years.

The lock-in period of ULIP has been increased to 5 years. If you are planning to surrender ULIP before 5 years, then you will have to surrender the charges as well but the amount will be paid post completion of the lock-in period.

Under ULIP, ‘fund value’ is the total amount of fund wherein the holder prefers to invest the funds.

The returns from ULIP are exempted under section 10(10D) of the Income Tax Act. However, if you discontinue ULIP before the lock-in period, you will not be entitled to any tax benefit.

Section 10(10D) of the Income Tax Act states that any bonuses earned along with the sum paid after the lock-in period/surrender of the policy/death of the insurer will be completely tax-free but will be subject to certain terms and conditions.

So, unit linked insurance plans provide you the benefits of good returns along with insurance coverage. They are like mutual fund investments but with an insurance cover. They also give you flexible benefits of partial withdrawals, switching and others and have tax advantages too. So, you can invest in a unit linked insurance plan if you are looking for investment returns along with insurance cover.