You can still get back your tax refund.

Get your belated tax returns filed before 31st March

e-Filing an income tax return form is scary, more so when you are doing it on your own. A simple mistake can make you a defaulter in the eyes of the Income Tax Department bombarding you with the Income Tax Notices, Penalties and Interest. Or in a simple situation just a loss of your income tax refunds.

In this guide we will explain to you what is ITR 1 form & how to e-file it? The article will also help you understand the taxation jargons asked in ITR 1, so that you can answer them correctly thereby avoiding the common mistakes that people make.

Let's get started!

As you already know Income Tax Return filing is done by way of submitting the income tax form to the income tax department. Different ITR forms are notified by the tax department depending on the source of your income. ITR 1 form commonly known as Sahaj is one such form. It is one of the most used forms in India. It is a simple form used for Income Tax Return filing & submitting your income, deductions and tax details to the income tax department.

This form can be filed by RESIDENT Individuals who have income upto Rs. 50 Lakhs in the Financial Year (F.Y.) 2019-20 i.e from 1st April 2019 to 31st March 2020 from the following: -

Further, in case where the income of your spouse, minor child, etc. is clubbed with your income, then this return form can be used only when your total income (after clubbing) also falls in the above specified categories.

This Return Form cannot be used by an individual whose total income for the F.Y. 2021-2021(A.Y. 2020-21) exceeds Rs.50 lakh or any of the following -

For Financial Year (Assessment Year 2020-21), the Government of India has introduced Form ITR-1 vide its notification date 03rd Jan 2020 and notification no. 01/2020 which has been further amended on 29th May 2020.

https://www.incometaxindia.gov.in/forms/income-tax%20rules/2020/itr1_english.pdf

https://www.incometaxindia.gov.in/hindi/forms/income-tax%20rules/2020/hnitr12020_hindi.pdf

Though ITR Form 1 looks like a simple form. But, while filling it, due caution should be taken.

ITR Form 1 is structured in five parts and two schedules for easy understanding. These are :

| Field | Description | Is it Compulsory to Fill?(Yes/No) |

|---|---|---|

| PAN | Permanent Account Number | Yes |

| Name | Enter your full name as per your PAN Card | Yes |

| Aadhaar Number | Providing Aadhaar Number is now mandatory while filing returns. Enter your 12 digit Aadhaar Number or 28 digit Aadhaar Enrolment ID in case you do not have your Aadhar with you .

Incase, you fall in the below mentioned category then filling of your aadhaar no is not mandatory :

|

Yes with few exceptions |

| Date of Birth | Enter your Date of Birth as per your PAN card in DD/MM/YYYY format | Yes |

| Mobile Number | Enter your valid mobile number, this would be used by the IT department for all communications. | Yes |

| Email Address | Enter your valid mobile number, this would be used by the IT department for all communications. | Yes |

| Address | Enter your current full address. This would be used by the IT department for all communications.

|

Yes |

| If filed in response to notice u/s | Select the applicable option, depending on whether the return filed is under section

|

Yes |

| Return filed u/s | There are various sections under which return is filed. These are :

|

Yes |

| Original Acknowledgement Number | If you are filing the revised return under section 139(5) or defective return u/s 139(9) is asked by the department, then write the Acknowledgement number and date of filing the original return in DD/MM/YYYY format. | Yes (In case of revision of returns) Yes (In case of revision of returns) |

| Date of filing of Original Return | ||

| Notice Number | Many times, we receive notice from the IT department even when we have filed ITR. So, if you have received any notice under section 139(9)/142(1)/148/, and filing your ITR in response to these, then enter the Unique No./Document Identification Number (DIN) and Date of such notice or Order in DD/MM/YYYY format. | Yes(If received notices) |

| If filed in response to notice u/s 139(9)/142(1)/ 148 enter the date of such notice | ||

| Nature of Employment | Choose the category of your employer from the drop down menu

|

Yes |

| If filed under 7th proviso to section 139(1) | If you are not otherwise required to file ITR but fall under any of these categories

|

Yes |

Note :- Loss cannot be carried forward to next year. ITR2 is to be used for all such purposes.

It includes details of all deductions claimed under Section 80C to 80U of the Act. These include investments, Mediclaim, LIC Premium, Contribution to Pension Account, Education Loan, Donation, etc. This part also includes the Taxable Income which comes after deducting the amount of Total Deductions from Gross Total Income. Read our Deductions Blog for knowing more about this section. Column for deduction under section 80EEA and 80EEB has been added from AY 2020-21 (FY 2021-22) in line with the new budget pronouncements.

This part also includes the details of all the bank accounts held in India at any time during the year for which the return is filed.

This includes all the Details of tax payments including Advance Tax and Self - Assessment Tax Payments. Advance Taxes and Self-Assessment challan deposited details are required.These are :

This includes the Details of Tax Deducted/Collected at Source on Income Other than Salary. These details can be based on Form 16 A issued by various Deductors in respect of interest income and other sources of income.

This schedule contains the following details:

This includes the details of total investments/ deposits/ payments made between 1st April 2020 to 30th June 2020 and the amount you wish to claim as deduction under chapter VIA out of these total investments

There is a verification section in which you need to mention your Name and your father's name. After completing the Verification Section, fill the date and Sign in the space given. Without a valid signature, your return will not be accepted by the Income Tax Department (If you submit ITR to the Income Tax Department offline).

In case, you e-file your return then you can sign with your digital signature. If you do not have a digital signature, submit your return and return sign a hard copy of ITR V and send it to CPC Bengaluru else e-verify it.

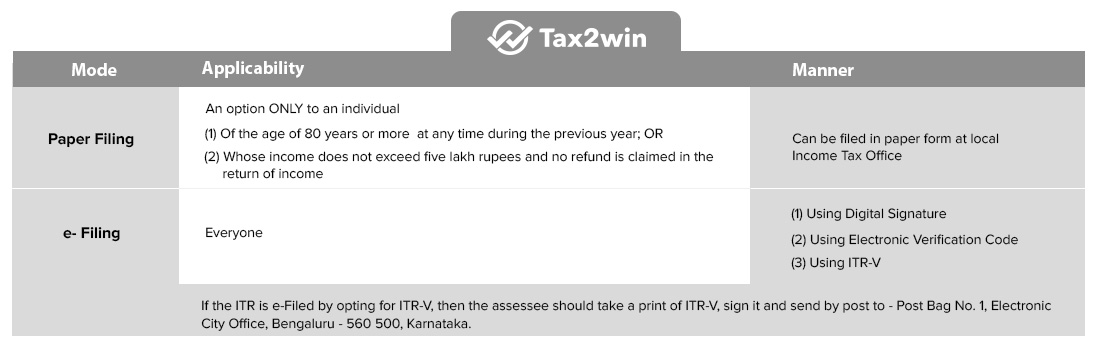

Form ITR – 1 can be filed with the Income Tax Department in any of the following ways:

For filing the form ITR1 online, follow the following steps:-

or

For the financial year, the due date for filing the ITR–1 is 31 December 2021.However the last date for income tax return filing for taxpayers whose accounts is 15th February 2022.

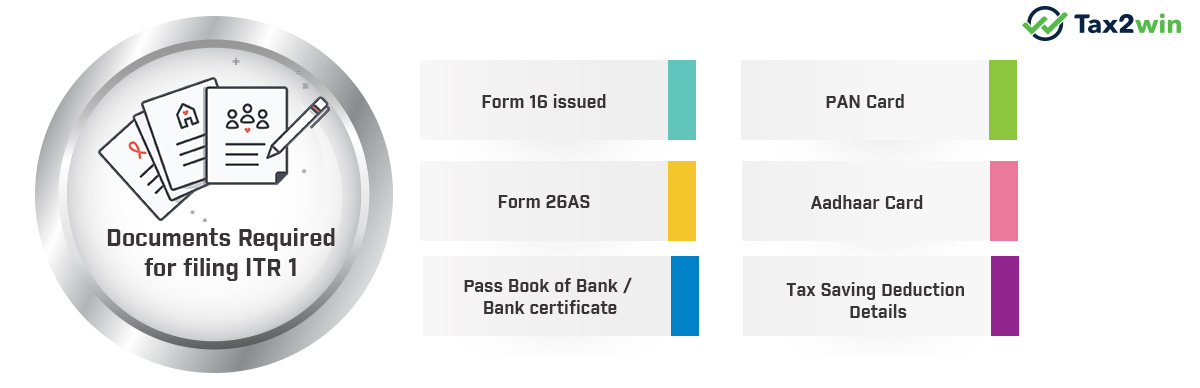

No documents are required to be attached when filing ITR 1. However, for filing, it is advisable to keep the following documents handy.

Major changes in ITR-1 for AY 2020-21 include fIling of Income Tax Return under 7th provision of section 139(1) under the following scenarios

Details of investment qualifying for deduction under chapter VIA with bifurcation of details of investment made during the period from April 1, 2020 to June 30, 2020 are required to be given while filing the ITR.

While filing ITR-1 under Nature of Employment, Government employees have been bifurcated as Central Govt. and State Govt. employees. Also, a new option “NA” has been added to the list. This option can be used by individuals claiming Family Pension, etc.

Happy Tax Filing from File My Tax online!!!

Start saving on taxes from today! Visit Your Tax Friend now!!

Well, ITR – 1 Form is an annexure less return, and you do not have to attach any documents along with your Income Tax Return.

Details of all savings and current accounts held at any time during the previous financial year must be declared under Part E – other information section of the ITR form .

Account numbers should be as per Core Banking Solution(CBS) system and dormant account (accounts which are not operational for more than 3 years) details are optional.

Furthermore, you have to specify the account that you want to use, in case of refund.

Yes, it is to be included before Part E – other information under the head Exempt Income(others) since dividend income from mutual funds is exempt under Sec 10(35).

| In case agricultural income<or = 5000 INR | File ITR 1 |

| In case agricultural income>5000 INR | File ITR 2 |

There is a limit put by the income tax department. Only 10 assesses can be registered using one mobile number and one email ID.

| Type of Income | ITR type |

|---|---|

| Salaried individual having income > 50 lakhs | ITR 2 |

| Income from business/profession | ITR 3 |

| Presumptive income u/s 44AD/44AE | ITR 4 (Sugam) |

Ans. Other Sources of income in ITR-1 includes the Interest Income from Savings Bank Account and FDR Interest Income, Post office interest income, Commission etc

Ans. If you have an income from both salary as well as capital gains then ITR 2 form needs to be filled.

Ans. Income Tax Return may be revised if the assessee has forgot to mention some income in ITR

Ans. Non Residents are not eligible to file the ITR-1. Normally, ITR -2 can be filed by the Non-Residents.

ITR on the income tax website can not be deleted, only revised return can be filed. Thus, you can file the ITR - 2 as a revision of the ITR. By doing this, your ITR 1 will be replaced by ITR 2 and it will be treated that you filed the ITR-2 as a Final ITR.

Ans. If any person having capital gain income or loss whether it is exempt or taxable, then ITR-1 cannot be filed. It needs to be disclosed under ITR-2.

Ans. Allowance under section 10 can be selected from the drop down box under the ITR form.

Ans. ITR 1 can be submitted in paper form by an individual of the age of 80 years or more at any time during the previous year.

Ans. If the total income of any person before allowing deductions under Chapter VI-A exceeds the maximum amount which is not chargeable to income tax then filing income tax return is mandatory.

As per current income tax slab the maximum amount not chargeable to tax is

| Category | Amount Exempt |

|---|---|

| Individuals aged below 60 years | Rs 2,50,000 |

| Individuals aged 60 & above but below 80 years | Rs 3,00,000 |

| Individuals aged 80 & above | Rs 5,00,000 |

Let’s understand with an example :

| Particulars | Amount |

|---|---|

| Gross Total Income | Rs. 3,00,000 |

| Deduction under chapter VI-A | Rs. 55,000 |

| Total Income/Taxable Income | Rs. 2,45,000 |

In the above example, say assessee is below 60 years of age. Then,he is required to file ITR since total income before allowing deduction exceeds the maximum amount which is not chargeable to income tax.

Ans. No document (including TDS certificate) should be attached to this ITR Form.